The industry keeps talking about “omnichannel” and “unified commerce” as if they were matters of experience, journeys, convenience, and touchpoints. They’re not. Omnichannel contains, first and foremost, a governance issue disguised as a design problem.

It didn’t start with consumers “asking for better experiences.” How do we even define what consumers want? Building models from trends is biased from the start. No. It started when payment and tech companies needed a new narrative to justify growth, attract capital, and hide fragmentation behind the promise of “seamlessness.”

Once we stop seeing omnichannel through the lens of experience, its political and economic logic becomes obvious. The illusion of unity starts to crumble.

Act I – The Manufactured Demand

Omnichannel retailing, and more precisely, omnichannel payments, were not born from customer demand. They were built to create one.

In the 2000s, merchants and banks treated payments as a back-office utility: necessary, costly, peripheral. By the mid-2010s, that model was exhausted. Banks began offloading their card-acquiring divisions, seeing them more as cost centres rather than value generators. What they sold, private equity soon repackaged as growth assets.

At the same time, consulting firms were busy building a new story on retail digitisation, which was labelled as inevitable and necessary. A 2015 report from Deloitte in Sweden declared that “a single-channel world is no longer sufficient,” defining the era’s dogma. Friction became the number-one enemy. Fragmentation of legacy systems was a sin.

Omnichannel emerged as the promise of redemption: the idea that connecting every store, website, and app could restore growth and relevance of the retailer’s proposition.

But this promise predated genuine consumer behaviour.

As banks exited, processors, gateways, and fintechs became vessels for return-driven capital

Online discourse inflated much faster than actual business adoption. Search data from Google Trends shows interest in “omnichannel retailing” climbing steadily from the mid-2010s onward, reaching record highs by the early 2020s, evidence of narrative inflation long before infrastructure caught up.

Omnichannel wasn’t a discovery, but rather a construction. As one Forbes editor wrote back in 2019, the term was “ill-defined” and “served up as the panacea for what ailed every struggling retailer.

Act II – The Financial Engine

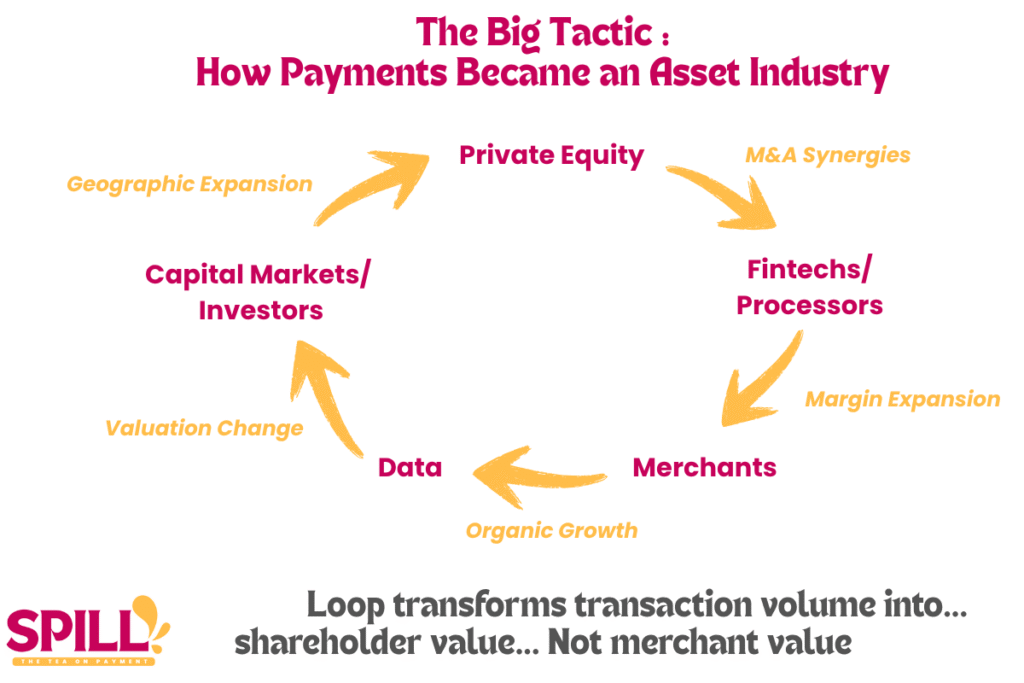

Once the concept existed, capital industrialised it.

Between 2010 and 2020, private equity and venture funds flooded into payments, turning infrastructure into an asset class to create maximum value in a short period of time. Consequently, the Valuation of Payments Businesses exploded.

By 2020–2021, Payments sector recorded more than a hundred M&A deals each year, illustrating a feverish consolidation wave.

As banks exited, processors, gateways, and fintechs became vessels for return-driven capital. To justify that inflow, they needed a story of limitless scalability, and omnichannel became the perfect one.

McKinsey’s How Value Creation Is Reshaping the Payments Industry (2017) captured that shift: control was moving from banks to fintechs, where growth was measured in multiples, not margins. As a result, consulting rhetoric followed. Omnichannel wasn’t just a strategy anymore; it was the benchmark of “digital maturity.”

It completely overshadowed the Omnichannel governance problem.

This narrative aligned perfectly with investor expectations and retailers’ struggle to reinvent. It sold the idea that linking e-commerce and physical retail could cut costs (fewer stores, leaner staff, smaller inventories) while boosting volumes through data insight and “seamless” fulfilment.

Click-and-collect became the symbol of that illusion: the store recast as an appendage to the website, a logistics node rather than a destination. As Deloitte wrote in 2015, “Omni-channel retailing, i.e. combining mobile, bricks-and-mortar and e-tailing, is the future of e-commerce.”

The sentence says it all: physical retail was no longer the centre of commerce; it had been redefined as the infrastructure of e-commerce. The hierarchy flipped, and governance followed.

By the late 2010s, this logic was fully embedded. Every major acquisition justified itself in the language of integration:

Verifone × Dimebox (2018) : orchestration infrastructure.

Worldline × Ingenico (2020) : “omnichannel merchant-services powerhouse.”

Nexi × Nets × SIA (2020–22) : “pan-European unified platform.”

All of a sudden, omnichannel was no longer about connecting experiences; it was about connecting revenue streams for payment service providers.

Act III – The Extraction Logic

By the 2020s, PayTech firms had perfected the model: sell dependency as simplicity.

What began as a story of “better” connection evolved into a structure of capture.

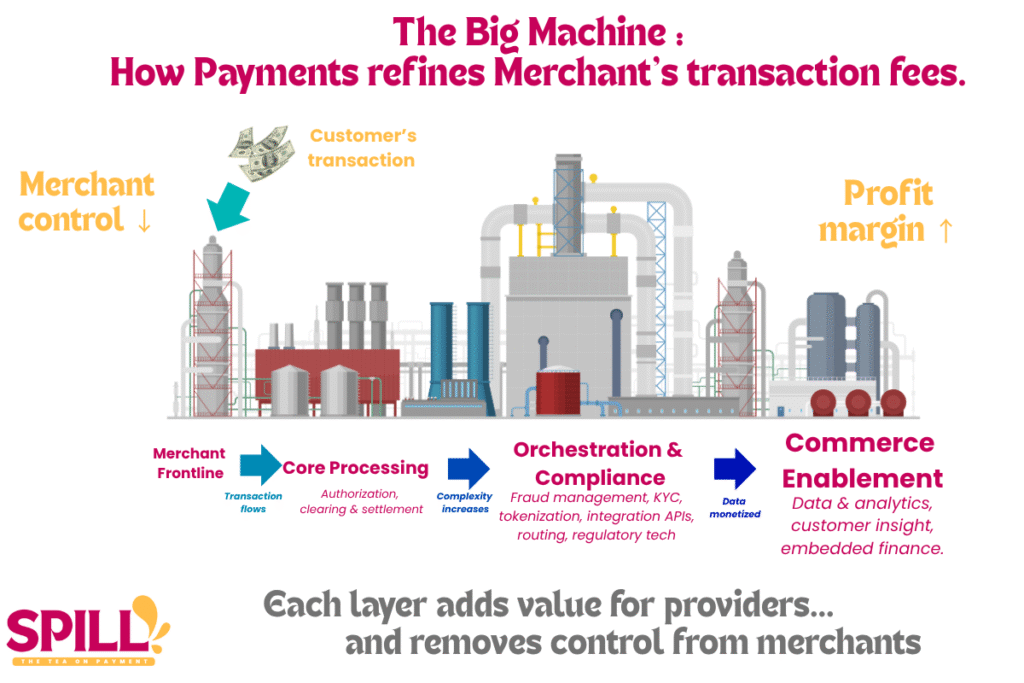

In the 2000s, payments were a technical necessity, the invisible plumbing of commerce. By the 2020s, they had become a rent-based system, monetising not the transaction itself but the layers surrounding it: data, loyalty, fraud, compliance, orchestration.

McKinsey’s Global Payments Report 2021 confirmed the transformation as well: around 80 % of merchant-service growth now came from “commerce enablement,” not core processing.

Adyen’s 2023 Retail Report echoed that message: merchants adopting Unified Commerce recorded eight percentage points higher revenue growth. Stripe’s 2024 announcements used the same logic, showcasing brands like Hertz and URBN as proof that unification equals performance.

But the hidden side of the model is cost and dependence, and PayTech firms rarely mention it.

Danish retailer Matas, for instance, budgeted up to DKK 100 million (≈ €13 million) for post-acquisition integration of KICKS, described as creating a “leading Nordic omnichannel beauty platform.” Most of that cost sits in system and data integration, a reminder of how expensive “seamlessness” really is.

Meanwhile, margins in European retail remain under pressure.

Across the continent, both grocery and non-grocery sectors have faced margin compression since 2019.

Industry analyses from McKinsey, EuroCommerce, and S&P show that while grocery EBITDA margins fell by roughly one percentage point between 2019 and 2024, most non-grocery retailers still struggle to regain pre-pandemic profitability.

Operational excellence has replaced governance as the new ideal, but that ideal comes at a price.

Merchants outsourced not just technology, but agency

Language became architecture, and soon every retailer felt compelled to “catch up.”

By 2017, 74 % of retailers declared omnichannel “critical,” yet only 8 % said they had achieved it successfully.

Even if the data is old, it shows how the Fear of Missing out phenomenon was evenly strong, whereas Omnichannel was barely emerging.

The more fragmented a merchant’s structure, the more convincing unification appears. PSPs positioned themselves as coordinators, absorbing complexity that firms couldn’t, or wouldn’t, manage. Complexity itself became a source of value. Omnichannel is a governance problem that providers could tackle and unify.

Even Forbes warned back in 2019: “The goal is not to be everywhere, nor is it to be seamless or unified.”

But by then, belief had already solidified into dogma. “Unified commerce” didn’t unify anything; it simply redistributed power.

Act IV – The Governance Vacuum

When omnichannel became institutionalised, the governance within Businesses blurred around that question.

Inside companies, fragmentation replaced strategy. The “customer journey,” once a design exercise, became an organisational battlefield. Everyone now owned a piece of it: Finance, IT, Sales, Marketing, Legal, Operations.

Data to Take Away

Ownership Shift

Between 2010–2020, the payment sector saw 100+ M&A deals per year, mostly driven by private equity.

Concentration of Power

By 2020, Europe’s top five processors controlled most transactions, while banks exited direct processing.

Where Growth Really Comes From

In 2021, 80% of merchant-service growth came from commerce enablement, not processing.

Illusion of Success

74% of retailers called omnichannel “critical,” yet only 8% achieved it successfully.

The Cost of “Seamlessness”

Matas budgeted up to DKK 100 million (~€13 m) to integrate KICKS into its “leading Nordic omnichannel platform.”

Roles multiplied: Project Managers, Omnichannel Leads, Heads of Payments, Chief Payment Officers, CX Directors, each with partial authority and no full ownership. Decision-making dissolved into procedures and gatekeeping, highlighting that omnichannel is a governance problem.

That vacuum was the perfect opening for payment providers to step in.

Their value proposition became governance itself: “We’ll unify what you can’t.”

But the downside was subtle; merchants outsourced not just technology, but agency. Whoever defines integration defines the rules.

This internal disempowerment mirrors Europe’s structural one. PSD2, GDPR, and EBA frameworks all aimed to harmonise markets but instead multiplied intermediaries. Europe built frameworks to follow, not visions to lead. Control over payment and customer data migrated upward, from firms to providers, and from providers to regulation. The merchant became an operator inside someone else’s system.

Governance didn’t vanish; it changed hands.

Beyond the Illusion

Omnichannel promised to connect experiences; instead, it created dependencies. It turned a coordination challenge into an asset class. Payments turned the Omnichannel governance problem into a financial product.

And because the illusion was profitable, everyone learned to speak its language: investors, consultants, and regulators alike.

But it would be interesting to see how models evolved, and better performing regions. In China, Retail never separated design, data, and payment, and therefore never needed to “unify” them again. Payment and commerce evolved as one ecosystem, not as layers trying to reconnect later.

The result is a better coherence, less fragmentation, and a more vivid retail commerce.

That is where this story continues.

You can read the previous episode of Unified Commerce illusion, on how the Payments Industry took advantage of the retail crisis.