Adyen, Nuvei, Checkout.com, Worldpay, Global Payments, all those Global Payment Providers are in China, more precisely in Shanghai. And yet, they’re not there to “conquer China.” That’s impossible.

For years, global payment providers in China have been described as outsiders facing a fortress. If you’re a foreign PSP, you can stand at the gate, admire the walls, and perhaps offer services to the occasional Western visitor. But getting in is way a challenge. Yet, the list of global players opening offices in Shanghai continues to grow. Why do all those companies go to China if the chances of succeeding are so thin?

The answer does not lie inside China, but rather outside in the growing appetite of Chinese retailers to go global without proper tools, and the inability of Europeans to position well here, not Western payments businesses. Nuance is important here.

The Fortress: Chinese payments are locked

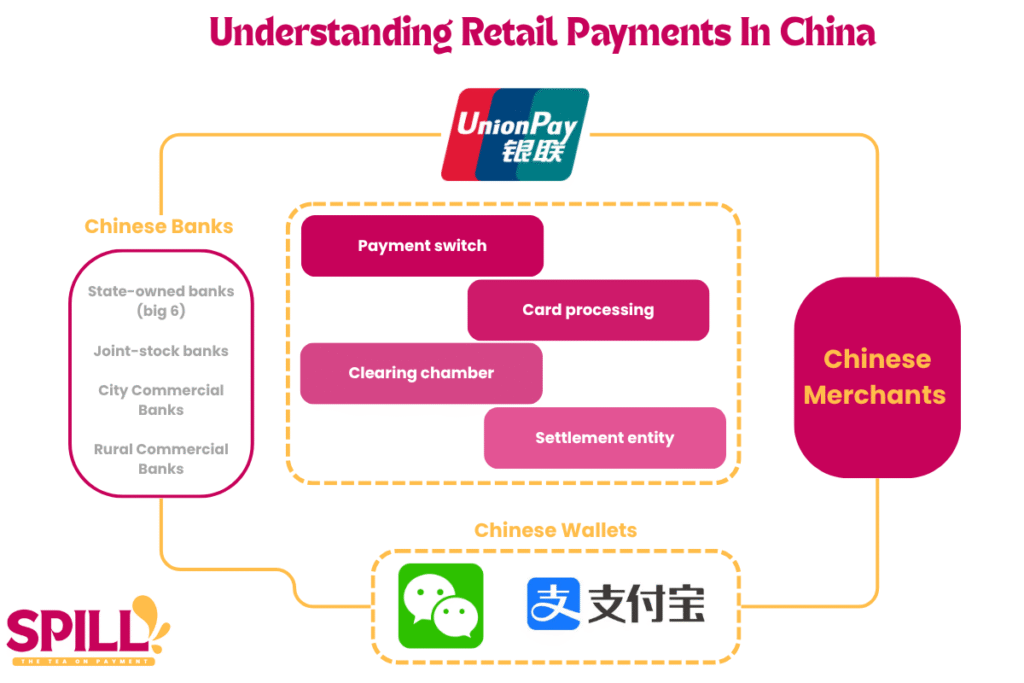

China’s domestic retail payments are dominated by two ecosystems: Alipay and WeChat Pay. These wallets have long overshadowed banks and card schemes. They don’t just process transactions; they are the number 1 choice for consumers with one specificity, radically different from the European landscape: they have embedded payments at their core. Cards are not there anymore; they play a second role.

UnionPay, the interbank card scheme, plays a different role. It provides the backbone for interbank settlement and clearing, but its capacity for innovation is limited. For Chinese banks, retail payments have never been a priority: too complex, too low margin, too small a portion of their business to justify heavy investment.

The number of banks competing in China is big: the big 6, the city commercial banks, the agricultural banks, and the foreign banks. The estimated number of them is between 2300 and 2400 banking institutions.

Foreign card schemes have tried to break in. Mastercard is the perfect example. After three years of procedures, it obtained the right to issue cards and clear domestic yuan transactions in 2023. And yet, as of today, operations haven’t even started.

Why? Because to operate domestically in China, Mastercard had to adapt to the Chinese model, which means taking responsibility for clearing and settlement as well, not just issuing and acquiring. That’s a world away from the role card schemes usually play in Europe or the US. Mastercard chose to set up a joint venture with NetsUnion Clearing Corporation, a local clearing entity, but even this carefully structured approach has not yet translated into real market activity.

This is why global payment providers in China cannot rely on their usual card-based revenue models. Cards are marginal in Chinese retail. The fortress is intact.

The Real Game: Chinese Retail Going Global

So why are global payment providers in China expanding their presence?

Because the real game isn’t about entering China like what Western businesses used to do 20 years ago. It’s about serving Chinese merchants as they expand abroad.

Over the last few years, Chinese retailers like Shein, Temu, and even TikTok Shop have accelerated their global push, flooding Western markets with new retail models, ultra-aggressive pricing, and massive logistics capacity.

Inside China, payments are streamlined to the extreme, with nearly no fat remaining, lean operations. Simple QR code system, instant settlements, embedded operations, full interoperability of ecosystems. Payments are background infrastructure, not a battlefield.

When these companies step into Europe or the US, they hit a wall of complexity:

- Fragmented acquiring landscapes

- A card-centric model they’ve never had to deal with

- Multiple schemes, regulations, authentication layers, and service providers

- A maze of compliance and settlement processes that make little intuitive sense from a Chinese perspective

This is where global payment providers in China step in.

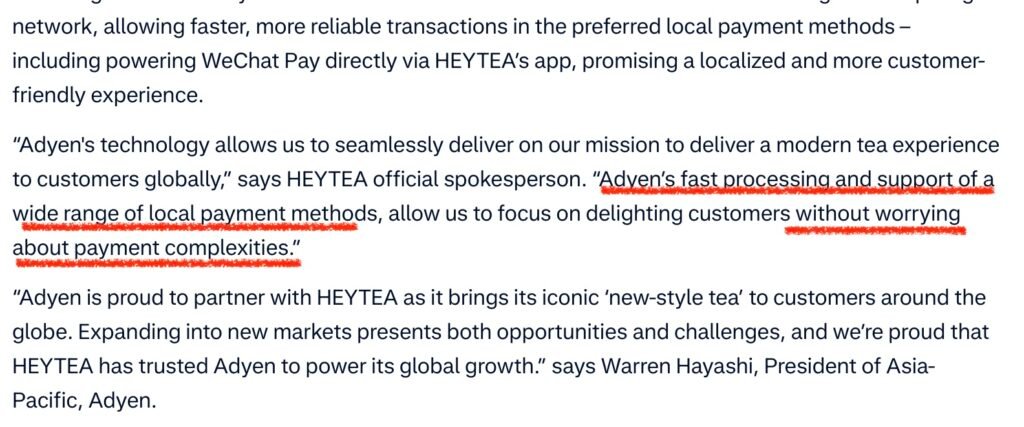

Their offices in Shanghai are not outposts for market conquest. They’re logistics hubs. Providers have strategically placed themselves to connect with Chinese merchants at the source, to help them navigate foreign payment systems, set up acquiring abroad, and handle the regulatory, scheme, and settlement puzzle on their behalf. The PR from Adyen about signing HeyTea is about handling “payment complexities”. It says all.

Shanghai is a launchpad.

Europe’s Blind Spot

Here’s where the story turns geopolitical.

In theory, Chinese merchants could rely on Chinese payment companies to accompany them abroad. After all, some of the Chinese businesses have a presence. But in practice, they often don’t and especially not in Europe.

Why? Because Europe makes it difficult.

Regulators are cautious, sometimes outright reluctant, to grant Chinese payment firms meaningful access or systemic weight in European markets. Chinese players are treated as potential geopolitical risks. The same doesn’t apply to American firms, which dominate Europe’s payment ecosystem without facing the same strategic scrutiny.

This is paradoxical. European institutions constantly speak of payment sovereignty, yet over 70% of European payment activity still depends on American infrastructure and schemes. The presence of Chinese payment players could be an opportunity to diversify dependencies, rebalance leverage, and stimulate competition and innovation.

Even a modest 5 to 10% market share gained by Chinese payment players under clear regulatory conditions, joint ventures, data safeguards, and technology transfer obligations could reshape the European payment landscape. Instead, Europe mostly chooses to look away. Or worse, to pinch its nose when China wants to invest.

The result is a passive posture. Europe doesn’t shape the game; it simply reacts to it, while global payment providers in China quietly build bridges between Chinese retail and Western markets.

A Strategic Gap… and a Trojan Horse

Western PSPs have understood something Europe hasn’t: the real action is in the flows generated by Chinese retailers abroad, not in chasing an inaccessible domestic market.

They’ve positioned themselves exactly where future transaction volumes are emerging. From Shanghai, they build bridges to support Chinese retailers’ international expansion, and in doing so, they make themselves indispensable.

But there’s more. These companies act as Trojan horses.

European and American PSPs like Adyen, Worldpay or Checkout.com are not simply “serving merchants”; they are strategic enablers of Shein, Temu, and others; the same companies that European politicians and retailers describe as threats.

No one accuses Adyen of “nurturing Chinese retail beasts,” yet its infrastructure powers them. Adyen, celebrated as a European champion and trusted by countless European merchants, is also digging their graves by supporting their fiercest competitors.

And here’s the hypocrisy: if Chinese retailers are truly seen as existential threats, why do European retailers continue to rely on the very same PSPs that fuel those competitors? They stay because the PSPs are efficient, global, and offer reach they can’t get elsewhere.

Europe talks sovereignty, but its infrastructure choices betray its words.

Staying focus instead of getting distracted

Global payment providers in China are not chasing a dream; they’re building bridges. China’s fortress won’t fall, but its merchants are going out, and whoever accompanies them controls a growing share of future payment flows.

Europe’s reluctance to engage with this reality is not neutrality. It’s a strategic gap, and through this gap, Trojan horses are already inside the walls.

For European retailers, the answer isn’t to cry foul every time Shein or Temu gains ground. It’s to get sharper, challenge their own operational models, and equip themselves with the right tools to compete. Complaining won’t stop the tide; strategic adaptation might.

For European regulators, the solution isn’t to overlook China, nor to close the gates entirely. It’s to play with the dragons: engage with Chinese Fintechs and their capacity to innovate, while setting clear, firm boundaries to protect European interests. Sovereignty isn’t built by looking away; it’s built by playing the game on your own terms.

This is not a story of exclusion, but of positioning and strategy. And right now, a bit as usual, Europe isn’t playing the strategic games, but waits in the middle.

In the coming weeks, I’ll dive into the case of HeyTea, a Chinese retail brand navigating this payment maze as it expands abroad. Its journey illustrates how these strategic tensions translate into concrete operational decisions and why Europe should pay closer attention.

You still can read the blog article, I did couple of months ago.