When Shein, Temu, or JD.com’s new venture JoyBuy storms European feeds, the reaction is pretty much the same: a mix of fascination and moral panic. Commentators rush to talk about low prices, labour, data, or geopolitics. We see the return of the “Yellow Peril”: they will eat us all. But they never mention that China unified commerce for real.

The undeniable success of Chinese businesses raises this question: how can they thrive in the most regulated, fragmented, and card-dependent market in the world? The answer cannot only be found in the discounts or algorithms, it also lies in the claim that Europeans said to have mastered: unified commerce.

The biggest irony is that Unified Commerce is a topic barely discussed in China, because China never had to discuss it. After all, it had already built it. Europeans, on the other hand, turned the concept into a flashy slogan. They added another layer of “digital transformation” to retailers already drowning in complexity. What China achieved through structure, Europe tried to mimic through governance outsourcing.

The success of Chinese e-commerce platforms in Europe reveals not only a cultural gap, but a structural one. While some payment businesses in Europe monetise fragmentation induced by Unified Commerce under the illusion of control, Chinese businesses have internalised governance to the point that payment has become almost invisible. In short, where Europe built an empire of schemes, China built an ecosystem of circulation. And when these two worlds collide, the illusion of European unity is exposed: the King is naked.

Europe’s False Unification : The Empire of Schemes

Europe’s version of “unified commerce” was born from a crisis. As physical retail lost its grip on consumers and digital channels multiplied, merchants were desperate to manage their stack. Payments, already sitting at the crossroads of every transaction, stepped forward with the perfect promise: simplify your world through us. One platform, one dashboard, one reconciliation file.

Unified commerce as a repackaged logic of the legacy model

But beneath that polished language stood an architecture that was never meant to unify anything: the four-party model of International schemes. The model rewards intermediation, not integration. Each transaction travels through a chain of players (issuer, acquirer, merchant, scheme, …). Each collects fees and enforces rules. The more layers, the more fees.

Europe’s regulatory culture only reinforced this pattern. PSDs, AML directives, EMV standards, PCI, all justified more actors, more checkpoints, more costs. “Innovation” became the art of dressing up this complexity just enough that merchants could still believe in the promise of simplicity.

Over time, payment providers stopped selling only processing technology and began offering governance of sales and “value-added services.” They promised merchants relief from the labyrinth while building the labyrinth higher. Adyen exemplifies this paradox: it offers unity by centralising gateway, acquiring, risk, and reporting functions. Yet it still runs entirely on the same scheme rails that create fragmentation in the first place. It doesn’t want to abolish the system; it repackages it. Nicely, indeed, but still on the same foundation.

A freestanding and administrative model to justify tollgate fees

The beauty of the model is that complexity feeds the business. The more rules and certifications appear, the greater the need for a “one-stop” provider to manage them. Compliance becomes a premium feature, not a shared good. Regulation, meant to contain market power, ends up reinforcing it. Governance itself becomes a commodity.

Private equity loves it because recurring fees look like stability. Merchants tolerate it because complexity disguised as simplification feels like progress.

In this configuration, “unified commerce” doesn’t unify anything fundamental. It turns governance into a product and monetises merchants’ dependency. The card schemes remain the invisible backbone, rewarding rigidity through volume. Their capacity to innovate is limited; they only need to ensure that everyone else’s innovation depends on them. Schemes are optimisers rather than radical innovators. And because the European industry’s revenue model is tied to those rails, any move toward genuine integration would undermine its own profitability.

Europe’s unification, in short, is administrative, not structural. It makes fragmentation livable, not solvable. It sells coherence without sovereignty. That’s the context into which China enters, and the contrast could not be sharper.

China’s Post-Payment World : The Governance of Integration

China’s payment revolution began with the absence. There were no entrenched schemes, no legacy acquirer networks, no culture of interchange fees. UnionPay existed, but more as an infrastructure backbone than a commercial empire. Visa and Mastercard were permitted mainly to serve Chinese travellers abroad, and, to a lesser extent, foreigners in China. The American duopoly never dominated domestic commerce.

Into this vacuum stepped two actors: Alibaba (the future Ant Financial) and Tencent (with WeChat Pay). They would redefine not only how people pay, as Western analysts like to say, but how commerce itself operates.

No legacy, bigger rooms to innovate

Their rise was opportunistic. Alipay began as a Taobao escrow service to solve trust in online transactions. Who could trust a UnionPay card with no meaningful fraud protection? Many cards were not even authorised for online use. WeChat Pay emerged later as a peer-to-peer wallet within a messaging app, a natural extension of virtual life, backed by Tencent, which had already spent decades mastering online communication since QQ’s launch in 1999.

Because there was no rigid system to integrate with, both platforms built everything themselves: wallet, acceptance, merchant onboarding, risk, compliance, identity, and even credit. They didn’t assemble partnerships; they designed an ecosystem under the eye of Chinese regulators who preferred domestic solutions to digitise a heavily cash-based economy. They achieved unified commerce in China for real.

This was China’s structural advantage. Instead of building around intermediation, it built around integration. Payment was not an industry to monetise but a layer of infrastructure connecting data, logistics, and behaviour. Revenue came not only from transaction fees but from the services payments enabled: marketing, lending, insurance, and cloud computing. In other words, payment became a utility that allowed commerce to flow.

A complete opposition to the European model

The result was a complete inversion of Europe’s model. In China, merchants don’t pay for “access” to governance; governance is embedded in the system. Compliance is absorbed at the platform level. The experience for merchants is radically cheaper and structurally simpler. They plug into an environment that already handles identity, risk, and settlement. The value of participation lies not in managing complexity, but in joining circulation. How can commerce in China be more unified than this?

This integration also redefined the relationship between consumers and merchants. On Alipay or WeChat, the payment moment fuses with communication, loyalty, and service. Buying a product, leaving a review, or applying for credit are all part of the same continuous interface. The merchant doesn’t rent tools from ten providers; they operate inside one infrastructure. It’s centralised, yes. But operationally coherent.

Once governance is internalised, payment itself dissolves as a category. You don’t think about paying inside WeChat; you just do your things. The transaction fades into the background of interaction. That’s what “post-payment” really means: when payment becomes so integrated that it no longer produces revenue or friction, it simply enables everything else.

That’s what Chinese consumers are proud of, and what Ant and Tencent’s “lifestyle app” narrative elevated to propaganda. I still remember how Western influencers who spoke Mandarin praised Chinese “superiority” in payments, and how well China unified commerce.

Europe still treats payment as a battlefield; China turned it into plumbing. In doing so, it resolved what Europe never dared to confront: that a truly unified commerce model demands unified governance.

But the system that works so smoothly inside China faces an existential contradiction when it crosses borders. Because when Chinese platforms expand abroad, they land on infrastructures whose entire business logic depends on keeping governance external.

Exporting Unity into Fragmentation : when Ecosystems Hit the Scheme Wall

When Chinese platforms enter Europe, they don’t just face consumers; they face an environment built to monetise fragmentation. Every licence, every API, every data-protection rule reinforces the separation between actors. What at home was one symbiotic organism must suddenly connect to foreign gatekeepers.

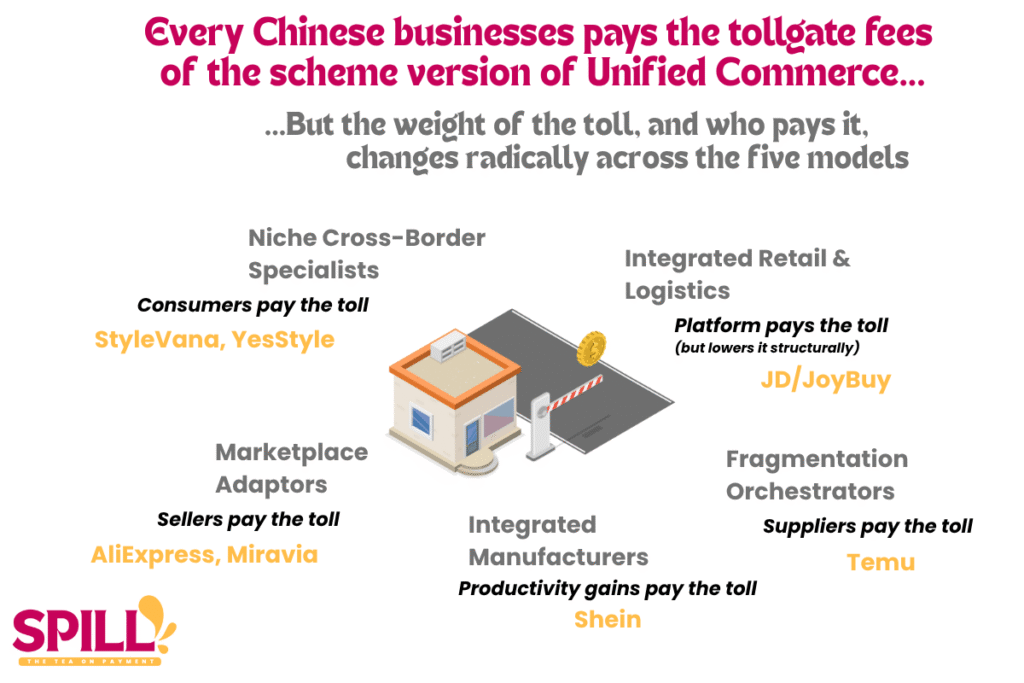

Their success is in mastering everything but the payments

Shein, Temu, AliExpress, and JoyBuy don’t exist in China. Chinese Businesses did not export their original model. It is impossible. They had to redesign their model for European constraints. In Europe, these companies can’t rely on integrated wallets or sovereign rails. They must use card networks, local acquirers, and payment service providers. Each layer adds cost and weakens data visibility. The Chinese model, based on total control of the merchant–consumer loop, breaks apart into procedural steps defined by others.

For these platforms, the challenge isn’t only competition, it’s translation. Their systems were designed to run on continuity; Europe forces discontinuity. They can’t own compliance, identity, or settlement as they do at home. They must lease governance from Western intermediaries, plug into networks built on rent-seeking, and obey a regulatory culture that treats every participant as a potential risk.

Yet even within these constraints, they succeed. Shein and Temu dominate because their efficiency lies upstream: in manufacturing intelligence, logistics compression, and algorithmic merchandising. Their power doesn’t come from payments; it comes from collapsing the rest of the value chain. But every European constraint reveals what they’ve lost: seamless data feedback, fluid loyalty systems, native trust mechanisms. They operate at full speed on a road filled with tolls. Toll-based logic doesn’t only affect giants.

Chinese Brands without Giant platforms pay the big price

For Chinese brands expanding westward, the gap between domestic coherence and international fragmentation becomes existential.

Take HeyTea, a wildly popular beverage chain in China whose app merges payment, ordering, loyalty, and community. In the PR from its Western payment partner (Adyen), the brand announced that it would “let the PSPs handle payment complexities.” The sentence sounds pragmatic but carries an entire tragedy: by outsourcing payments, HeyTea also outsources its governance, and with it, the very integration that defines its model. What was a real unified commerce in China becomes way more complex to handle in the West.

China’s platforms may adapt, but in doing so, they expose Europe’s architecture for what it is: a carefully maintained network of dependencies. Europe calls it resilience; in practice, it’s a system that cannot let go of control because its profitability depends on it.

The Mirage of Unified Commerce, Exposed

The story of Shein, Temu, isn’t about China invading Europe. It’s about two incompatible logics of commerce meeting face to face. Europe built a market where governance (especially in Payments) is externalised, standardised, and monetised. China built one where governance is internal, infrastructural, and largely invisible. Each system has its risks. Europe’s rigidity breeds dependency; China’s integration breeds concentration. But only one of them has made payment irrelevant. Follow my eyes eastward.

Europe’s dependence on scheme logic guarantees that every layer of unification must pass through a toll. Each new regulatory wave adds sophistication without sovereignty. Payments remain the backbone of power and profit, not the foundation of circulation.

By contrast, China’s duopoly of Ant Financial and Tencent turned payment into the least interesting part of commerce precisely because it ceased to be the only profit centre. They earn elsewhere because payment is no longer the limit of their business.

When Chinese ecosystems operate in Europe, they force the continent to look in the mirror. What we call “unified commerce” is in fact the management of silos, a choreography of intermediaries pretending to be an integrated system. The success of Chinese platforms doesn’t threaten Europe; it merely reveals how little unity there ever was.

Europe’s problem is not that its payment system failed; it’s that it succeeded too well in keeping itself indispensable. Governance became the business model, and once Providers monetise governance, the freedom and creativity of Retailing become increasingly difficult.

China solved payments by dissolving them. Europe still builds them to feel in control.